Abstract

Abstract

Abstract

The software was written and published in 2002, vibe code

modernized in 2026.

Bsengine calculates the fair value of European-style options based

on current stock prices. Additionally, it provides several key

computations, including Greeks, spread, break-even, Omega,

Gearing, and Rho. It utilizes the option pricing algorithm

developed by F. Black and M. Scholes, the architects of the

Black-Scholes model. The software was written in C on a SUN

workstation and was primarily designed to function as a

back-office processor. The code has been optimized for the Linux

operating system. While the author has successfully built the

software on Windows, this was done for testing purposes only and

is not recommended for production use due to known operating

system limitations.

Design Goals

The initial motivation for developing this software was a personal requirement for a system capable of receiving data from a stock exchange server to evaluate warrants based on a specific risk profile. A secondary design goal was to create a system independent of slow online banking websites often cluttered with advertisements. The third and most important reason was the discovery of inconsistent product information and miscalculations on various broker websites. Rather than relying on existing online banking systems, I prefer to invest based on my own calculations. Bsengine is designed for the industrial processing of batch data, such as automatically populating broker websites (similar to Swissquote or Consors). The bsengine kernel features a clean CLI interface and a modular, high-speed design. This concept allows the software to operate unattended as part of a larger batch processing workflow. Feel free to develop a Gtk+ frontend for the kernel if desired.

Post-processing Notes

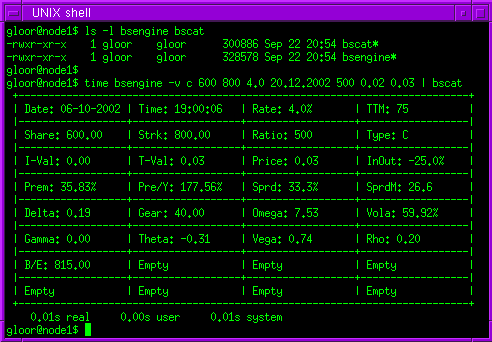

Once the mathematical calculations based on the derivative pricing

model are complete, bsengine writes its results to stdout

(typically the computer screen). The standard output is a

token-separated data string, which can be easily parsed by

productional batch processing sub-processes. Using this feature,

the output can be loaded into a relational database management

system (RDBMS), such as a MySQL

database server, for further processing. I have also

developed an additional application called bscat (bsengine

catalog), which reads bsengine's output via a Unix pipe and

formats it into the human-readable layout shown in the screenshot

above.

Technical Notes

The bsengine kernel and bscat are written entirely in C and are

easily portable to other Unix environments or operating systems

that support pipes. The software was developed on a SUN Sparc 5

running GNU/Linux. To calculate implied volatility, a fast

approximation formula was necessary. I utilized the

"Newton-Raphson" algorithm to numerically determine volatility

using the generalized Black-Scholes model. The "Manaster and

Koehler" algorithm handles the initial values for iterations,

which is the primary reason bsengine is extremely fast at

computing option prices. Bsengine has undergone extensive testing

using real-time data from trading systems. This software is ready

for production use; however, please note that the bsengine package

is published under the GNU

General Public License, which means it is provided without

any warranty.

Future Plans and Additional Features

No software is ever truly finished; this version of bsengine is a

snapshot of my current development source tree (Work in Progress).

I plan to expand its capabilities once I secure access to a

favorable or free stock exchange interface. Finding an adequate

data provider is a challenge, which is the main reason further

development is currently on hold. As option pricing requires

real-time data, current development focused on speed and

reliability. If you have suggestions, comments, or contributions,

please feel free to contact me via email.

Examples of bsengine and bscat in Action

gloor@node1$ ./bsengine -h

bsengine 1.0.0 - Black/Scholes Option pricing (UNIX)

written by Marc Gloor

<marc_dot_gloor_at_u_dot_nus_dot_edu>

usage : bsengine [options] [arguments]

example: bsengine -v c 6024.2 8000 4.0 20.10.2002 500

0.02

0.03

options are:

-h show

help

-v

compute implied volatility

-r show

release

-p

compute fair price

-v arguments (in

order):

-p

arguments (in order):

-1st Call/Put flag

[c/p]

-1st

Call/Put flag [c/p]

-2nd Underlying price

[dec]

-2nd Underlying price [dec]

-3rd Strike price

[dec]

-3rd

Strike price [dec]

-4th Interest Rate %

[dec]

-4th

Interest Rate % [dec]

-5th Maturity

[dd.mm.yyyy]

-5th Maturity [dd.mm.yyyy]

-6th Options ratio

[dec]

-6th

Options ratio [dec]

-7th Bid price

[dec]

-7th

Volatility % [dec]

-8th Ask price [dec]

In production environments, you can populate a relational

database using the following command:

gloor@node1$ ./bsengine -v c 6024.2 8000 4.0 20.10.2002 500

0.02

0.02

Example of the semicolon-separated data output:

22-09-2002;20:08:12;C;6024.20;8000.00;500;28;4.0%;0.03;55.63%;-24.7%;...

Example of bsengine and bscat working together (e.g., for a CGI script):

gloor@node1$ bsengine -v c 6024.2 8000 4.0 20.10.2002 500

0.02

0.03 | bscat

+---------------------------------------------------------------------------+

| Date: 22-09-2002 | Time: 20:09:08 | Rate:

4.0% | TTM:

28 |

|------------------+------------------+------------------+------------------|

| Share: 6024.20 | Strk:

8000.00 | Ratio:

500 | Type:

C |

|------------------+------------------+------------------+------------------|

| I-Val: 0.00 | T-Val:

0.03 | Price:

0.03 | InOut:

-24.7% |

|------------------+------------------+------------------+------------------|

| Prem: 33.05% | Pre/Y:

1179.91% | Sprd: 33.3% |

SprdM:

119.8 |

|------------------+------------------+------------------+------------------|

| Delta: 0.04 | Gear:

401.61 | Omega:

16.77 |

Vola: 55.63% |

|------------------+------------------+------------------+------------------|

| Gamma: 0.00 | Theta:

-1.52 | Vega:

1.50 | Rho:

0.18 |

|------------------+------------------+------------------+------------------|

| B/E: 8015.00 |

Empty

|

Empty

|

Empty

|

|------------------+------------------+------------------+------------------|

|

Empty

|

Empty

|

Empty

|

Empty

|

+---------------------------------------------------------------------------+

Data Field Descriptions

Date: Timestamp

date

Pre/Y: Premium per annum

Time: Timestamp

time

Sprd: Spread

Rate: Interest

rate

SprdM: Spread Move

TTM: Time to

maturity

Delta: Delta

Share: Share

price

Gear:

Gearing

Strk: Strike

price

Omega: Omega

Ratio: Options

ratio

Vola: Implied volatility

Type: Type

(Call/Put)

Gamma: Gamma

I-Val: Intrinsic

value

Theta: Theta

T-Val: Time

value

Vega:

Vega

Price: Fair option

price Rho:

Rho

InOut: Moneyness

(In/Out)

B/E: Break-even

Prem: Premium

Benchmarks

In computational simulations, the pricing of 20,000 options was

completed in seconds. Performance may vary depending on hardware

specifications and current system workload. The binary has been

optimized for Linux (stripped code).

License

This distribution is licensed under the GNU General Public

License.

Download the Latest Release

bsengine-1.1.0-src.tar.gz

[.tar.gz, 83kb]

bsengine-1.1.0-statbin.tar.gz

[.tar.gz, 580kb]

If you require further assistance, please let me know.

$Id: bsengine.html,v 1.23 2026/04/26 09:26:08 gloor Exp $ |